Calculating COGS helps you price with clarity, understand profitability and make changes based on numbers, not instinct.

When putting together an income statement for your business, one of the most important steps is figuring your cost of goods sold (COGS), which represents all of the direct costs associated with producing the goods you sell during a specific period.

Accurately calculating and tracking your business‘ COGS is crucial, since it’s the portion of your expenses you have the most immediate control over.

Subtracting COGS from total income tells you your gross profit, which can help you decide which farm enterprises to expand or scale back, which production methods to use, and even how to get your product to market. Here’s how it works and what you need to know.

What is my cost of goods sold (COGS)?

Your cost of goods sold (COGS) are any expenses your business made that went directly into producing goods for sale.

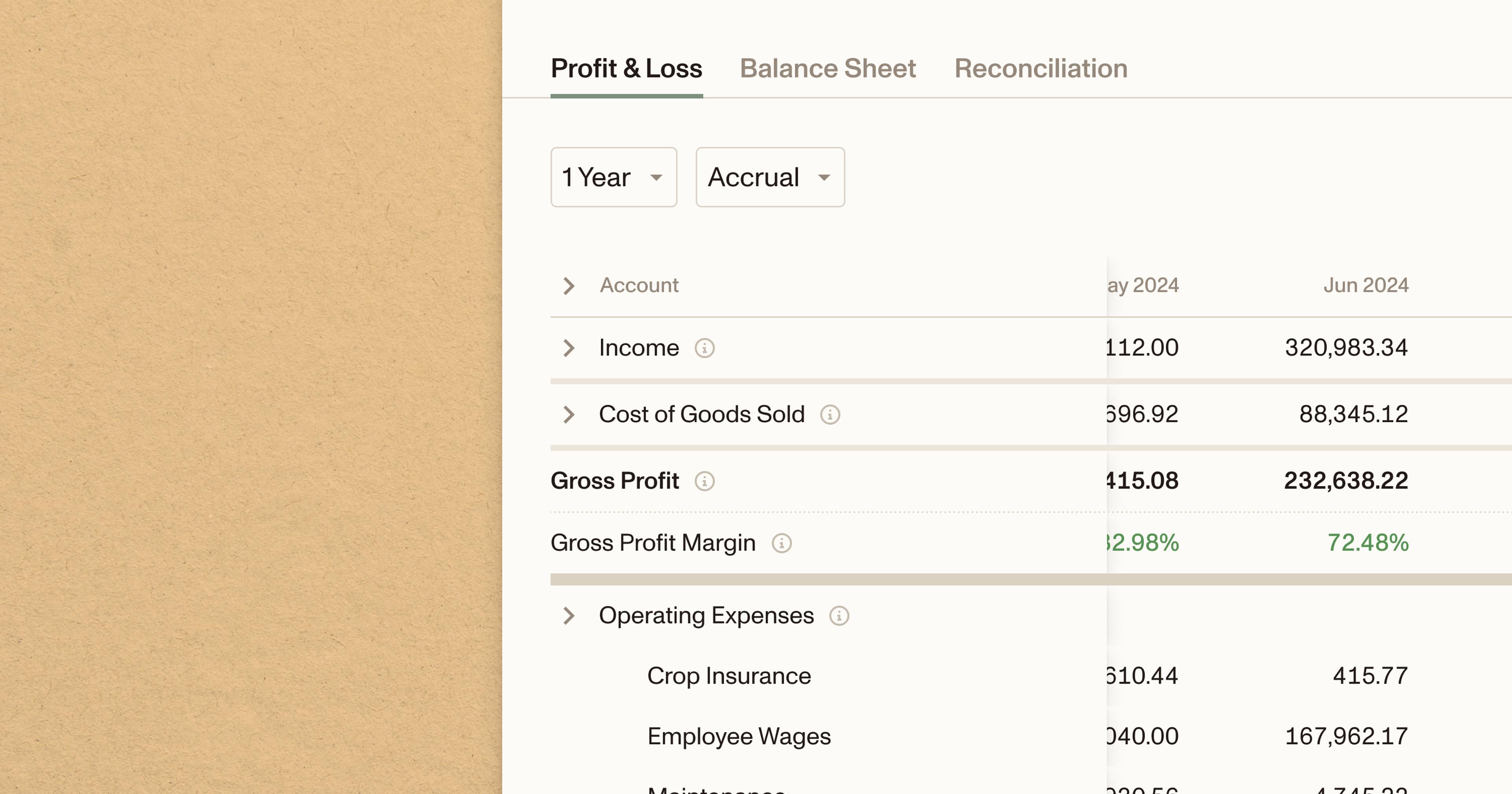

On an income or profit and loss statement, COGS is often listed right after income, before any other expenses. Those other expenses are often less directly tied to production—e.g. utilities, marketing and administrative costs—and are referred to as “operating expenses.”

COGS: Examples

Grain, seed and straw

Salt, minerals and protein

Forages and pasture rental

Herd replacement

Veterinary medicine and supplies

Death loss

Breeding costs and bull leasing

Fertilizer

Production labor

Manure removal

Trays, boxes, bags and labels

Operating Expenses: Examples

Marketing costs

Fuel and utilities

Hauling

Transportation

Maintenance and repairs

Subscriptions

Office expenses

Retailer fees

Distributor fees

Insurance

Commissions

If you’re ever wondering whether an expense qualifies as a COGS, consider whether it’s directly related to producing goods, and whether decreasing or increasing production would decrease or increase that cost.

If you raise more beef, for example, you’ll need to increase the amount of feed you use, making that a COGS expense.

How do I calculate COGS?

Accounting software like Ambrook can help you calculate COGSs automatically, but if you’re starting from scratch using pen and paper or a spreadsheet-based income statement, you’ll have to calculate COGS manually.

To calculate total COGS for your entire operation, you’ll need to add up all of your variable or ‘direct’ costs, which are costs that increase with each additional unit of output.

For cow-calf operations, for example, this might include feed (pasture, hay or rations), supplements, depreciation, labor and breeding costs, while for feedstock production it might include seed and fertilizer, fuel and labor.

Inventory costs are a big part of COGS, and how you account for them matters. For example, choosing a costing method like FIFO or WAC can affect which inventory gets ‘used up’ and recognized as COGS first.

For consistency, you’ll also need to decide whether to include costs like family labor and your own unpaid labor in COGS, or whether you’ll include only cash costs.

Cost of goods sold formula

If we express the above as a formula, we get:

COGS = Raw materials used + Direct labor costs + Any other variable costs used in production

This is how accounting systems like Ambrook handle COGS, but you might also sometimes see COGS defined using the following formula:

COGS = (Beginning inventory + Purchases) – Ending inventory

This formula reflects how inventory under an accrual accounting systems works, and ensures that COGS reflects what actually got sold, not just what was produced.

Why is COGS important?

1. Profitability insight

Subtracting COGS from revenue gets you gross profit, which can help you determine whether a certain enterprise in the business is profitable. If your COGS are creeping up, margins can shrink, and changes might be in order.

2. Pricing and strategic decisions

Knowing your true cost of producing a calf, backgrounding a feeder or harvesting a ton of hay helps you make better pricing decisions and target a specific level of return on your spending.

3. Cost control and benchmarking

Having a consistent COGS methodology allows you to compare your numbers year to year or against industry benchmarks, which can surface important trends.

4. Investment and expansion decisions

If you know your cost structure, you can better assess the impact of adding a new enterprise to your business.

5. Tax and accounting clarity

Under accrual accounting, COGS affects your taxable income and proper matching of revenue and expenses.

How does COGS work for a cash basis business?

Accrual accounting matches costs like COGS to the revenue they help generate, which prevents margins from being distorted by timing differences between when expenses are paid and when income is earned.

Most U.S. farmers operate on a cash-basis accounting system, however, which means only expenses actually paid in cash during the year are counted. If you don’t track inventory, COGS essentially becomes a subtotal of the direct costs purchased specifically for customer work. Whether the expense was paid by invoice, check, or credit card, the deductible amount for taxes is simply what was paid in cash during the year.

For tax returns, start with the totals from your income statement, assuming it is prepared correctly. From there, apply any required adjustments to arrive at the final tax-deductible amounts, which are often slightly lower than the book totals.

Know your numbers with Ambrook

Ambrook is the complete financial platform for your agricultural operation, providing a complete set of books and detailed financial insights.

With time-saving bookkeeping automation features, automatically-generated financial reports, streamlined bill pay and invoicing, and other powerful accounting and financial management tools, Ambrook takes the guesswork out of running your business.

Want to learn more? Schedule a demo today.

Want to learn more about Ambrook?

This resource is provided for general informational purposes only. It does not constitute professional tax, legal, or accounting advice. The information may not apply to your specific situation. Please consult with a qualified tax professional regarding your individual circumstances before making any tax-related decisions.