If you pay someone more than $600 in rents, royalties, veterinary fees or barter over the course of the year, you might have to file a 1099-MISC. Here’s how.

If you pay someone who isn’t your employee above a certain amount in the calendar year for the use of rental property, royalties, attorney fees, or barter, you’ll probably have to file a 1099 Form to report it to the IRS.

There are 22 different 1099 forms, each used to report a different payment type. Form 1099-MISC, Miscellaneous Information, covers a wide range of payment types, including rents, royalties, veterinary fees, crop insurance proceeds or barter. Here’s how it works.

What is Form 1099-MISC?

IRS Form 1099-MISC, Miscellaneous Information is a tax form that businesses must file whenever they pay someone above a certain threshold in rents, royalties, crop insurance proceeds, barter, veterinary fees, attorney fees and other similar miscellaneous payments.

For 2025 that threshold is $600, and for 2026 it’s $2,000. (See more on payment thresholds below.)

Some examples of businesses that might have to fill out and file a 1099-MISC include:

A farmer paying a clinic for veterinary services

A rancher reporting a barter exchange with a neighbor

A business owner paying their commercial landlord for retail or office space

In addition to filing with the IRS, you must also send a copy of 1099-MISC to the recipient of the payment.

Taxpayers who receive a copy of 1099-MISC must then report that income on their own tax return using forms like Schedule F (Form 1040) and Form 8995-A. Some examples of businesses that might receive a 1099-MISC include:

A farm operating a wedding events space receiving a rental payment

A rancher who rented their machinery or vehicles to another business

A neighbor you bartered with

1099-NEC vs. MISC: What’s the difference?

Before 2020, taxpayers used 1099-MISC to report a much broader range of payments, including cash payments to independent contractors and other non-employees for services like repairs, improvements, farm labor, consulting services, and so on.

In 2020, the IRS (re)introduced an old tax form called Form 1099-NEC, Nonemployee Compensation, which is specifically for reporting payments to non-employees, like independent contractors who are subject to the self-employment tax.

Today, Form 1099-MISC is no longer used to report non-employee compensation, however it’s still used to report payments for things like medical and legal services (more on that below).

Which types of payments do I have to file a 1099-MISC for?

‘Miscellaneous’ covers a broad range of different payment types, including:

Rents (Box 1)

Royalties (Box 2)

Prizes and awards, including certain non-government grants (Box 3)

Any fishing boat proceeds (Box 5)

Medical and health care payments (Box 6)

Crop insurance proceeds (Box 9)

Gross proceeds paid to an attorney (Box 10)

If you pay land rental payments to a real estate agent or property manager instead of the property owner, you generally don’t have to report that on 1099-MISC. (They’ll have to use 1099-MISC to report rent paid over to the property owner themselves.)

Payments for hauling grain or livestock and payments for supplies and materials like feed, seed, fertilizer and fuel generally don’t require a 1099-MISC.

Payments to corporations (including LLCs treated as a C or S corporation) don’t need a 1099-MISC, with the exception of medical and health care payments and attorney fees.

Use 1099-MISC only to report any payments connected to your business. If you pay your neighbor to paint your house, for example, that’s a personal expense that you don’t need a 1099-MISC for.

What are the 1099-MISC reporting thresholds for 2025 and 2026?

Up to 2025, the threshold for filing a 1099-MISC was $600. Then in July of 2025, the One Big Beautiful Bill Act (OBBBA) changed the reporting threshold for 1099-MISC for 2026 to $2,000, which will be adjusted for inflation for 2027 and beyond.

This means that any payments made after December 31, 2025 are no longer subject to the old $600 threshold: they’ll either be subject to the new $2,000 threshold for 2026, or inflation-adjusted thresholds for 2027 and beyond.

Remember that miscellaneous payments include barter

Just like cash payments, payments you make to other businesses with bartered goods or services must also be reported using box 3 of 1099-MISC.

When making a barter exchange, remember to keep a record of the cost of goods being bartered or traded, the transaction date, and the fair market value (FMV) of the transaction at the time of exchange.

What do I need before filling out and filing 1099-MISC?

In addition to information about the payment type and amount, you’ll need the recipient’s name, contact information and taxpayer identification number (TIN) to properly file a 1099-MISC. You can get this information by giving them a copy of Form W-9.

If the recipient doesn’t get back to you with a filled out W-9 and TIN, you’ll have to withhold taxes from their payment at the backup withholding rate of 24%. (More on that below.)

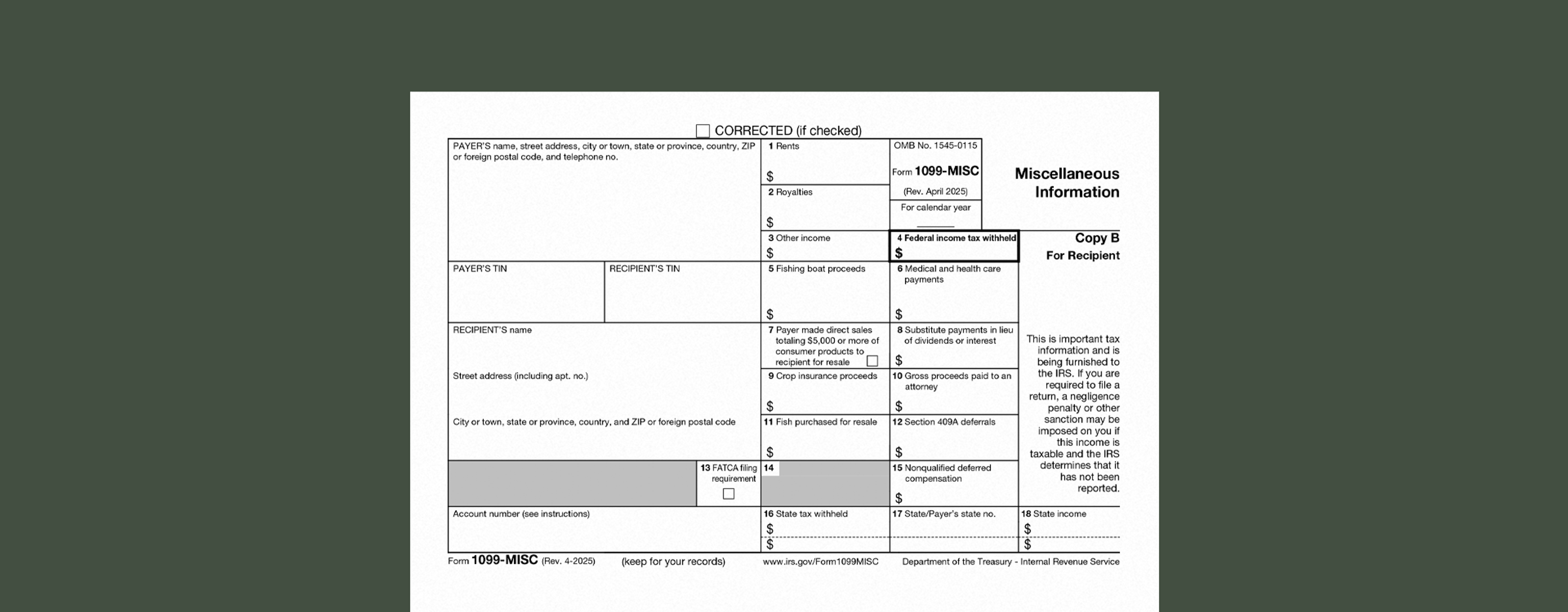

Form 1099-MISC: a box-by-box breakdown

On the left hand side of each 1099-MISC you file, enter the payer’s (your) name and contact information, your taxpayer identification number (TIN), your recipient’s TIN, and the recipient’s name and contact information.

If you’re filing more than one information form for each recipient, include an account number at the bottom of the form. This can be a checking account number, savings account number, brokerage account number, serial number, loan number, policy number, or any other unique number you assign that payee to distinguish their account.

Box 1: Rent payments

This box should include total rent payments the payer made to the recipient, and can include payments like:

Rent paid for commercial or office space to a landlord or property owner.

Machine or vehicle rental fees paid to the property owner. If the rental includes an operator fee, prorate and report that fee in box 1 of Form 1099-NEC.

A pasture rental fee paid to the property owner for use of grazing land.

If you receive a copy of 1099-MISC, you’ll have to report this amount on Part I, Schedule E (Form 1040) or Schedule C (Form 1040).

Box 2: Royalties

This represents total royalty payments made by the payer to the recipient.

Royalty payments can include fees paid to property owners for the right to extract oil, gas and minerals, as well as payments for the use of intangible property such as patents, copyrights, trade names and trademarks.

If you receive a copy of 1099-MISC, you’ll have to report this amount on Part I, Schedule E (Form 1040).

Box 3: Other income

This box is used to report any income that is not reportable in any of the other boxes on Form 1099-MISC, and can include payments like:

Prizes and awards that are not for services performed

Payments of bartered goods or services to another business

Compensation paid in a calendar year to an H-2A visa agricultural worker who did not provide a valid TIN

Payment of a deceased employee’s wages to an estate or beneficiary

If you receive a copy of 1099-MISC, report this amount on Schedule 1 (Form 1040).

Box 4: Backup withholding

This box is used to report backup withholding. If you’re the payer and the recipient hasn’t furnished you with their TIN, you must withhold tax from their payments and file Form 945 to report it. The current backup withholding rate is 24%.

If you receive a copy of 1099-MISC with an amount in this box, you may have to complete and send Form W-9 to the payer.

Box 5: Fishing boat proceeds

This box is used by fishing boat operators to report the recipient’s share of proceeds from the sale of a catch. (See the instructions to 1099-MISC for more on reporting fishing boat proceeds.)

If you receive a copy of 1099-MISC, report this amount on Schedule C (Form 1040).

Box 6: Medical and healthcare payments

This box is used to report medical payments to physicians and other suppliers or providers of medical or health care services, including veterinarians. Don’t include payments to pharmacies for prescription drugs.

If you receive a copy of 1099-MISC, report this amount on Schedule C (Form 1040).

Box 7: Direct sales

Check this box if you (the payer) made $5,000 or more in sales to the recipient on a buy-sell, deposit-commission, or other commission basis for resale (i.e., ‘direct sales’). You may also use box 2 on Form 1099-NEC to report this, however you must only use one form.

Box 8: Substitute payments

This box is used by the payer to report payments of $10 or more to a broker for a customer in lieu of dividends or tax-exempt interest.

Box 9: Crop insurance proceeds

This box is used by insurance companies to report crop insurance proceeds paid to farmers (unless the farmer has informed the insurance company that expenses have been capitalized under Section 278, 263A, or 447).

If you receive a copy of 1099-MISC with an amount in this box, report it on Schedule F (Form 1040).

Box 10: Attorney payments

This box is used to report payments to an attorney for legal services.

Box 11: Fish purchased for resale

This box is used by fish resellers to report payments to fishermen. (See the instructions to 1099-MISC for more info.)

Box 16-18: State tax withheld

These boxes contain any state income tax withheld from payments, the payer’s TIN, and the taxable income for the tax withheld.

How do I file Form 1099-MISC?

You have to file multiple copies of Form 1099-MISC, each one with a different recipient and due date:

The first copy, “Copy A,” goes to the IRS and must be filed by February 28, 2025 if filing on paper and March 31 if filing electronically.

The second copy, “Copy B,” goes to the recipient so they can report that income on their own taxes.

You might also have to file two other copies: “Copy 1,” which goes to your state or local tax department, and “Copy 2,” which goes to the recipient so they can send it to their state or local tax department, if necessary.

In addition to the extra copies of 1099-MISC, you’ll also have to file Form 1096, which acts as a kind of ‘cover sheet’ for all of your information returns (which includes all of the different 1099 forms).

When does each copy of 1099-MISC have to be sent out?

If you’re filing a 1099-MISC for payments you made, you must furnish a copy to the recipient (Copy B) by January 31, 2025.

You should receive a copy of Form 1099-MISC for any payments you received in 2024 by early February 2025. If you don’t, follow up with the payer about getting one issued.

For 1099 forms filed in 2025, there’s a $60 late penalty per form if you file within 30 days of the deadline, which goes up to $130 if you’re more than 100 days late, $330 if you file after August 1st, and $660 if you intentionally fail to file.

If you fail to file and the income goes unreported, the payee could also be subject to a penalty equal to 20% of the unreported income.

1099-MISC deadlines for 2025:

| 1099-MISC, Copy B (For Recipient) sent to payees: | January 31 |

|---|---|

| 1099-MISC, Copy A (For IRS), if filing on paper: | February 28 |

| 1099-MISC, Copy A (For IRS), if filing electronically: | March 31 |

Late filing penalties:

| If you file Copy A or B within 30 days of the deadline: | $60 per form |

|---|---|

| If you file Copy A or B within 100 days of the deadline: | $130 per form |

| If you file Copy A or B before August 1: | $330 per form |

| If you intentionally fail to file: | $660 per form |

Kickstart Your Tax Season with Ambrook

Ambrook’s category tags correspond directly to each line on Schedule F, making it easy to compare your tax return to your records and saving you hours of work during tax season.

With time-saving bookkeeping automation features, automatically-generated financial reports, streamlined bill pay and invoicing, and other powerful accounting and financial management tools, Ambrook doesn’t just make filing your taxes easy: it takes the guesswork out of running your business. Want to learn more? Schedule a demo today.

Want to learn more about Ambrook?

This resource is provided for general informational purposes only. It does not constitute professional tax, legal, or accounting advice. The information may not apply to your specific situation. Please consult with a qualified tax professional regarding your individual circumstances before making any tax-related decisions.