If you pay wages to your employees, you’ll probably have to pay federal unemployment taxes (FUTA) and file IRS Form 940. Here’s how to do it properly.

When eligible workers lose their jobs, they might receive some form of unemployment compensation. The money to fund these payments comes from unemployment taxes paid to states and the federal governments, and the federal portion of these taxes is called the Federal Unemployment (FUTA) Tax.

If you employ a certain number of workers or pay your employees above a certain amount over the calendar year, you’ll need to file Form 940, the Federal Unemployment Tax return, to report your FUTA payments.

What is Form 940?

Unlike social security, federal income tax and medicare, the FUTA tax isn’t withheld from employees’ paychecks–employers must pay it themselves. To report these payments to the IRS, employers have to file the FUTA tax return, Form 940, which is filed once a year.

The FUTA tax only applies to the first $7,000 paid to each employee. The official FUTA tax rate is 6.0%, but employers who pay their state unemployment taxes on time generally receive a credit of 5.4% when they file Form 940, resulting in a net tax rate of 0.6%. (However, this doesn’t apply to ‘credit reduction states’ like California, New York and the U.S. Virgin Islands.)

Who must file Form 940?

If you answer “Yes” to any one of these questions, you must file Form 940:

Did you pay wages of $1,000 or more to household employees, $1,500 or more to regular employees, or cash wages of $20,000 or more to farmworkers in any calendar quarter during 2024 or 2025?

Did you have one or more employees for at least some part of a day in any 20 or more different weeks in 2023 or 20 or more different weeks in 2024? Count all full-time, part-time, and temporary employees. However, if your business is a partnership, don’t count its partners.

Did you employ 10 or more farmworkers during some part of the day (whether or not at the same time) during any 20 or more different weeks in 2024 or 20 or more different weeks in 2025?

When is Form 940 due?

Your Form 940 for 2024 is due on January 31, 2025. If you’ve deposited the FUTA tax you owe for the year in full and on time, however, you have until February 10 to file.

While you must file Form 940 annually, if your Form 940 tax liability at the end of any quarter exceeds $500, you must deposit the tax by the end of the next month. If you owe a total of $500 or less during the first three quarters, you can carry that amount over until the next quarter.

| If your undeposited FUTA tax is more than $500 on… | Deposit your tax by… |

|---|---|

| March 31 | April 30 |

| June 30 | July 31 |

| September 30 | October 31 |

| December 31 | January 31 |

You might be subject to penalties or interest if:

A correct Form 940 is not filed by the due date

The tax due with the return is not paid

You didn’t make timely payments of the FUTA tax during the year

How to file Form 940, the FUTA tax return

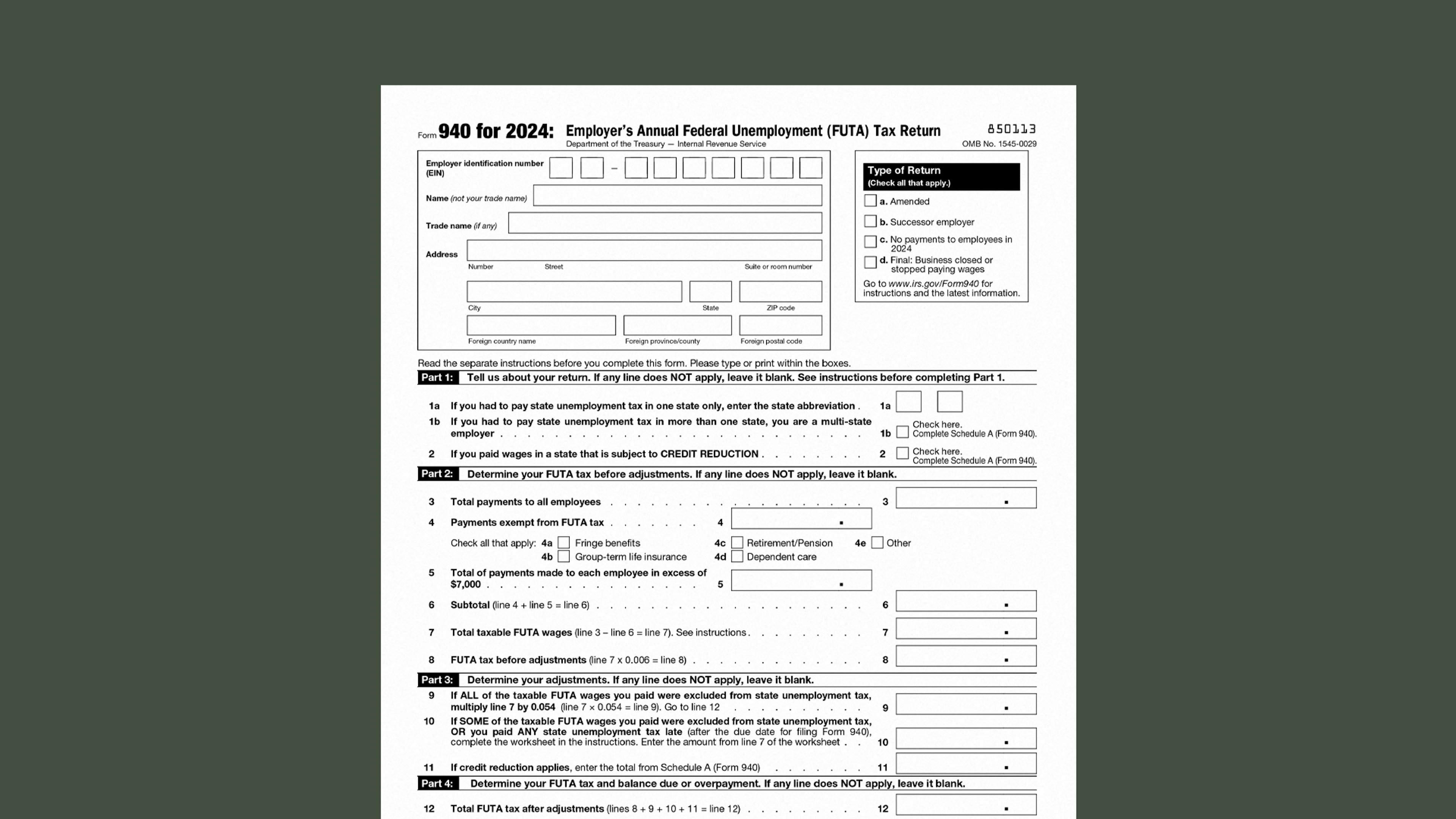

To start, you’ll provide some basic information about your business, including your employer identification number (EIN), name, trade name (if any), and business address.

You’ll also specify if you’re filing an amended return, if you’re a successor employer, if you didn’t make any employee payments in 2024, and/or if this is your final FUTA tax return (i.e. you’re shutting down the business or not paying wages anymore).

Part 1: Are you a multi-state or credit reduction state employer?

Here you’ll report whether you’re a multi-state employer (Lines 1a and 1b), and also whether you paid wages in a credit reduction state. (The credit reduction states for 2024 are New York, California and the U.S. Virgin Islands.)

If you’re a multi-state employer and/or you paid wages in a credit reduction state, you’ll have to complete and attach Schedule A (Form 940).

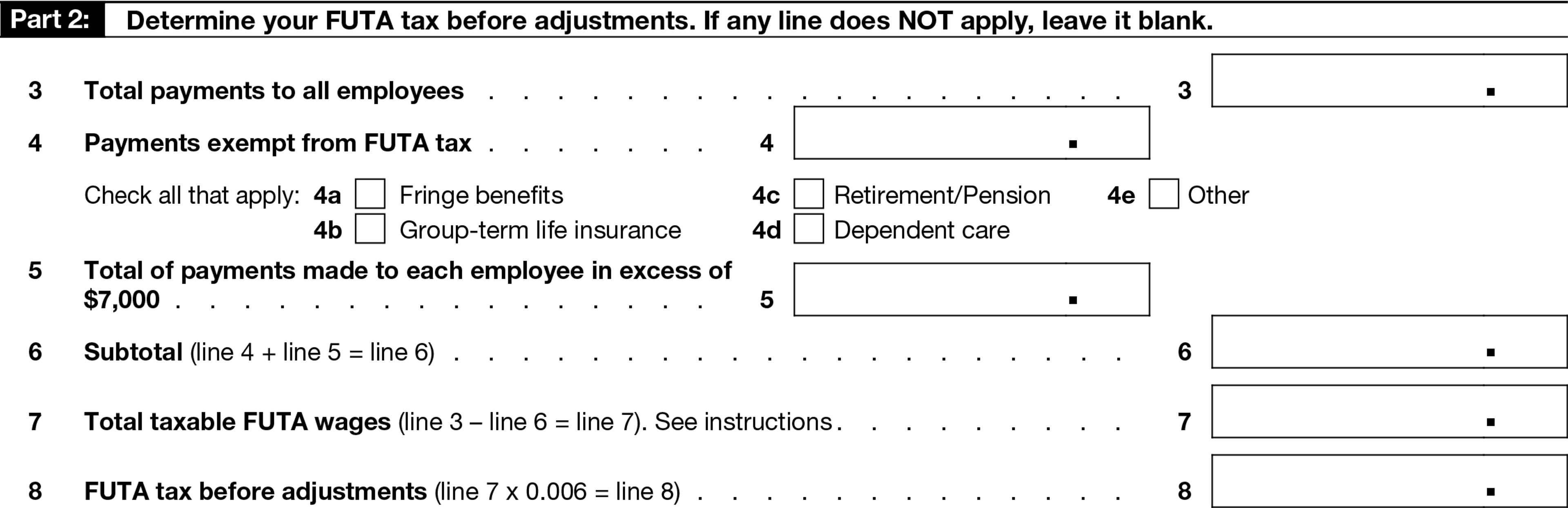

Part 2: Calculating FUTA tax before adjustments

Here you’ll determine your total FUTA tax for 2024 before adjustments. The amount you record on Line 3 should include all payments made to employees, including:

Wages, salaries, commissions, fees and bonuses

Vacation allowances

Dismissal pay and severance pay

Reportable tip income

Some payments are not taxable for FUTA and can be subtracted from total payments on Line 3. These exempt payments are entered on Line 4 and can include:

Workers’ compensation paid for injury or sickness

Wage payments to the employer’s children if they are under 21

Wage payments to the employer’s parents

Non-cash payments to farmworkers and household workers

Only the first $7,000 of wages for each employee is subject to FUTA tax, and amounts over $7,000 paid to each employee can be subtracted from total payments on Line 3. Any amount over $7,000 paid to each employee is recorded on Line 5.

Keep in mind that if you buy an existing business and retain the employees, you may count the wages paid by the previous employer to the continuing employees when computing the $7,000 limit.

Part 3: Calculating FUTA tax adjustments

If all of the FUTA wages you paid were excluded from state unemployment tax, multiply the amount on Line 7 by 0.054 and record the resulting amount on Line 9. (This line isn’t applicable if your state assigned you an employer rate of 0%.)

If some FUTA wages were excluded, or you paid any state unemployment taxes late, use the worksheet labelled “Worksheet—Line 10” in the instructions to Form 940 to figure your credit and record it on Line 10. (Don’t attach the worksheet to Form 940.)

If you paid FUTA wages that were also subject to state unemployment taxes in a credit reduction state (NY, CA or VI in 2024), enter the total from Schedule A (Form 940) on Line 11.

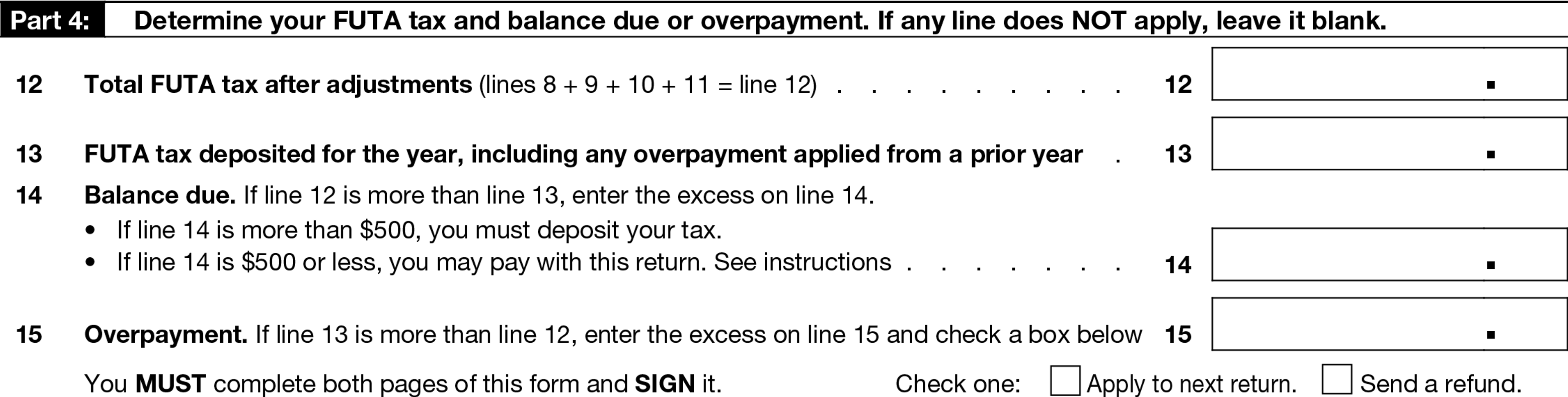

Part 4: Calculating total FUTA overpayment or balance due

Here you’ll add together the amounts you calculated in the previous two sections to figure your total FUTA tax after deductions (Line 12) and compare it to the total FUTA tax you’ve deposited for the year (Like 13) to show whether you have any outstanding FUTA tax due (Line 14).

If the amount on Line 14 is more than $500, you’ll have to pay the total amount by January 31st. If it’s $500 or less, you can pay when filing Form 940 (either on January 31st or February 10th).

Part 5: Reporting your FUTA tax liability

In this section you’ll report your FUTA tax liability for each quarter if the total amount reported on line 12 is more than $500. If it isn’t, skip this section.

Part 6 and 7: Signature and paid preparer information

Complete these sections if you’re paying someone (e.g. an accountant, representative, tax preparer) to help you prepare this tax return and you want to authorize them to speak to the IRS about this Form 940 on your behalf. This is also where you or whoever is responsible for filing Form 940 signs their name.

Make Tax Season Less Taxing with Ambrook

Ambrook’s category tags correspond directly to each line on Schedule F, making it easy to compare your tax return to your records and saving you hours of work during tax season.

With time-saving bookkeeping automation features, automatically-generated financial reports, streamlined bill pay and invoicing, and other powerful accounting and financial management tools, Ambrook doesn’t just make filing your taxes easy: it takes the guesswork out of running your business. Want to learn more? Schedule a demo today.

This resource is provided for general informational purposes only. It does not constitute professional tax, legal, or accounting advice. The information may not apply to your specific situation. Please consult with a qualified tax professional regarding your individual circumstances before making any tax-related decisions.