To deduct depreciation, Section 179, Bonus Depreciation or amortization on your taxes, you’ll have to file IRS Form 4562. Here’s how it works.

Staying on top of deductions can be a great way to lower your tax bill, but not all business expenses can be deducted immediately. Expenses that benefit your business for more than one year like vehicles, equipment and buildings must be ‘depreciated’ or spread out and deducted over multiple years.

Form 4562, Depreciation and Amortization is the IRS form that you’ll use to claim depreciation on your taxes, and it’s also where you’ll claim special deductions like Section 179 and bonus depreciation. Here’s what you need to know before you do.

How do depreciation and amortization work?

Most of the inputs a business spends money on are ‘used up’ over a period of time. To encourage economic activity, the tax code allows businesses to deduct some of these expenses on their tax returns.

For expenses that are used up within one year, deductions are simple: you write off their entire cost in one go on your annual tax return. But for machinery, equipment, buildings, and other capital expenses that take longer than one year to ‘use up’ due to wear and tear, depreciation is used to recover those costs instead, by spreading the deduction out over multiple years.

‘Amortization’ is just depreciation for intangible assets, which for farming businesses can include things like farm lease agreements, purchased goodwill and livestock breeding rights.

How long does it usually take to depreciate or amortize something? It depends in part on which depreciation system you choose. The following table summarizes the recovery periods for some typical farm assets under both the General Depreciation System (GDS) or the Alternative Depreciation System (ADS):

Farm Property Recovery Periods (In Years)

| Assets | GDS | ADS |

|---|---|---|

| Cattle (dairy or breeding) | 5 | 7 |

| Farm buildings | 20 | 25 |

| New farm machinery and equipment | 5 | 10 |

| Used farm machinery and equipment | 7 | 10 |

| Tractor units (over-the-road) | 3 | 4 |

| Truck (heavy duty, unloaded weight 13,000 lbs. or more) | 5 | 6 |

| Truck (actual weight less than 13,000 lbs.) | 5 | 5 |

What is IRS Form 4562?

Form 4562, Depreciation and Amortization is the IRS form you’ll use to claim depreciation and amortization on your taxes. It’s also the form you’ll use to claim Section 179, which is a special tax rule that allows small businesses to instantly write off more than a million dollars in qualifying property – up to $1,220,000 in 2024 – in the year that it’s purchased. You might file Form 4562 if:

You just built a new 10,000 square foot poultry production building and want to claim first-year depreciation for it

You’d like to continue claiming depreciation for a tractor you purchased three years ago

You purchased a new truck and want to claim the Section 179 deduction for it

When is Form 4562 due?

You should file Form 4562 whenever you file your annual tax return with the IRS. This might be March 1 if you’re a farmer who didn’t pay estimated tax by January 15th of this year, April 15th, or October 15th if you filed Form 4868 for a six month extension.

Form 4562: what to do before filling it out and filing

Before claiming depreciation using Form 4562, you’ll have to decide how you want to depreciate assets you want to claim depreciation for.

Farmers have a wide range of depreciation systems and methods available to them, which can make this process complicated and difficult to navigate without the help of a professional.

We cover some of the basics in our guide to depreciation and MACRS, but to do this properly you’ll definitely want to speak to an accountant or tax lawyer.

Once you and your tax advisor have settled on a depreciation convention and method, you’ll have a few important data points for each asset, which you’ll then need to record on Form 4562:

Asset value

Month and year placed in service

Recovery period for that asset

Depreciation convention and method

The depreciation deduction you and your tax professional calculated for this year

If the assets you’re claiming depreciation for are used for both personal and business use, you’ll need to provide a percentage of business use for those assets backed up by records.

If you’re claiming depreciation for a vehicle you use for both personal and business use, you’ll need to have that vehicle’s mileage log handy as well.

Form 4562: how to fill out and file properly

The 2024 PDF version of Form 4562 is two pages long and divided into six parts.

Parts I and II are where you’ll claim the Section 179 deduction and the special depreciation allowance, also known as “bonus depreciation.”

Part III is where most of the action happens: it’s where you’ll actually claim depreciation for your assets.

Part IV is a summary of all the different amounts you’re claiming on Form 4562 (a bit confusing considering summaries usually go at the end).

Part V is for “listed property,” which is what the IRS calls property that can be used for both business and personal purposes.

Part VI is for amortization, which is just depreciation for intangible assets.

Part I: Election To Expense Certain Property Under Section 179

Lines 1-5

There’s a limit to how much you can deduct under Section 179 ($1,220,000 in 2024) and that amount starts to “phase out” dollar for dollar when your total purchases pass a certain threshold, which is $3,050,000 in 2024.

Enter the Section 179 limit for the year you’re taking the deduction for on line 1, the total cost of the property you’re deducting on line 2, the deduction threshold on line 3, any reduction in the limit on line 4, and the total resulting Section 179 limit on line 5.

Lines 6-9

On these lines you’ll list out each piece of property you’re taking the Section 179 deduction for, as well as any “listed property,” which is property that can be used for both business and personal purposes. (See Part V for more on listed property.)

Lines 10-13

If you couldn’t write off the total purchase price of a piece of property using Section 179 last year and decided to carry some of that amount over to this year, enter that amount on line 10.

The total value of the Section 179 deduction can’t exceed your total income for the year: if your total income is lower than the amount you calculated on line 5, enter that on line 11.

Record your total Section 179 deduction on line 12, which is just the sum of lines 9 and 10, or the amount on line 11, whichever is smaller.

Finally, if you’re carrying over any disallowed deductions to next year–which would equal the sum of lines 9 and 10, minus line 12–record that amount on line 13.

Part II: Special Depreciation Allowance and Other Depreciation

If you acquired property after September 27, 2017, and you placed it in service after December 31, 2023 and before January 1, 2025, you can deduct 60% of its cost using bonus depreciation, also known as “special depreciation allowance.”

Once you’ve calculated the special depreciation allowance by multiplying the basis of the property by the applicable percentage, record the resulting amount on line 14.

If you use the unit-of-production method to depreciate your property, or any other method that isn’t MACRS, enter the depreciation amount on line 15. (You’ll also need to attach a separate sheet to Form 4562 that includes how you arrived at that number–see the instructions to Form 4562 for more.)

You’ll use line 16 to record all other forms of depreciation, including ACRS property and property placed in service before 1981.

Part III: MACRS Depreciation

The Modified Accelerated Cost Recovery System (MACRS) is what most taxpayers must use to depreciate their property.

As discussed above, choosing a depreciation system can get complicated, and you’ll want to consult a tax professional before doing so. Once you have settled on a system, you’ll use Part III to write off the depreciation you calculate for each asset.

Section A

Use lines 17 and 18 to record depreciation for assets you placed in service before the year you’re filing your taxes for. If you purchased a new truck for your business and placed it into service three years ago, for example, you’ll record the depreciation deduction you’re claiming for that truck here.

Section B and C

Assets have different recovery periods depending on what kind of asset they are, and also depending on whether you use the Alternative Depreciation System (ADS) and the General Depreciation System (GDS) to depreciate them.

Generally speaking GDS has a shorter ‘recovery period,’ or length of time over which the assets are depreciated. You can find a longer comprehensive table of common farm assets with their ADS and GDS recovery periods in our guide to depreciation and MACRS.

In Section B, you’ll use lines 19a-i and columns b-g to record the depreciation deduction for all your GDS asset types grouped by recovery period, as well as the convention and method for each one.

‘Conventions’ determine when exactly the recovery period for an asset begins and ends, which can affect how much you depreciate in the first year.

‘Methods’ like the declining balance method and the straight line method determine how aggressively the asset will be depreciated over time (read more in our guide to depreciation).

In Section C you’ll repeat the same process you went through for Section B for your ADS assets.

Part IV: Summary

Here you’ll add together the depreciation calculated in the previous sections, and also the amount you record in line 28 in the next section (concerning “listed property,” which is property that can be used for business and personal purposes), to calculate total depreciation claimed for all assets.

For information about the uniform capitalization rules of section 263A and line 23, see Regulations section 1.263A-1.

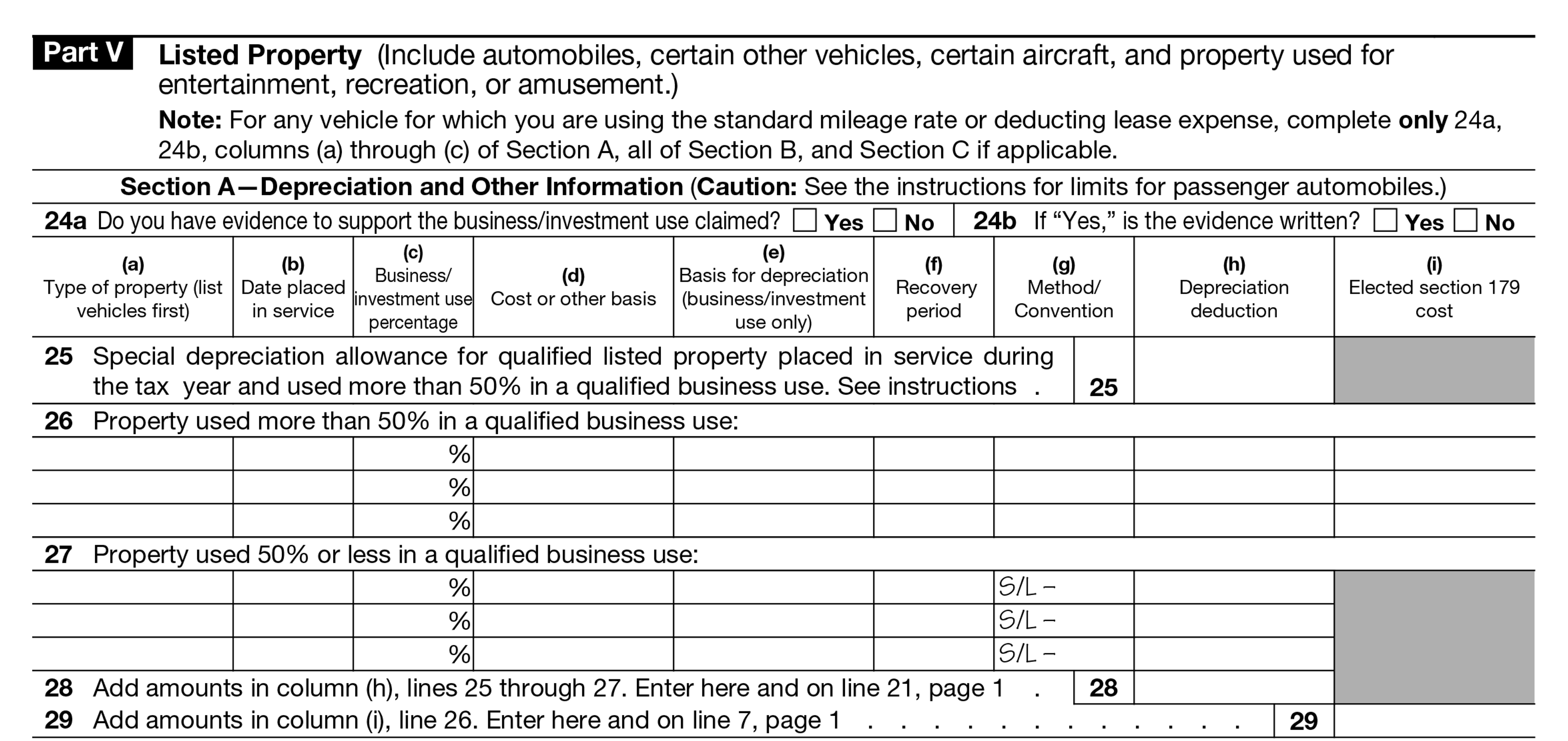

Part V: Listed Property

Here you’ll record depreciation for any assets you use for both business and personal use, or “listed” property. (Remember that any business use you claim for listed property will need to be supported by written records.)

Section A—Depreciation and Other Information

Use line 25 to record any bonus/special depreciation you’re claiming for listed assets.

Use line 26 and columns a-i to record property types, service date, cost, business percentage, recovery periods, methods, conventions, depreciation, and elected section 179 costs for assets you use more than 50% of the time for business.

Use line 27 and columns a-i to record the same information for assets you use less than 50% of the time for business, and lines 28-29 to come up with a total deduction amount for the section.

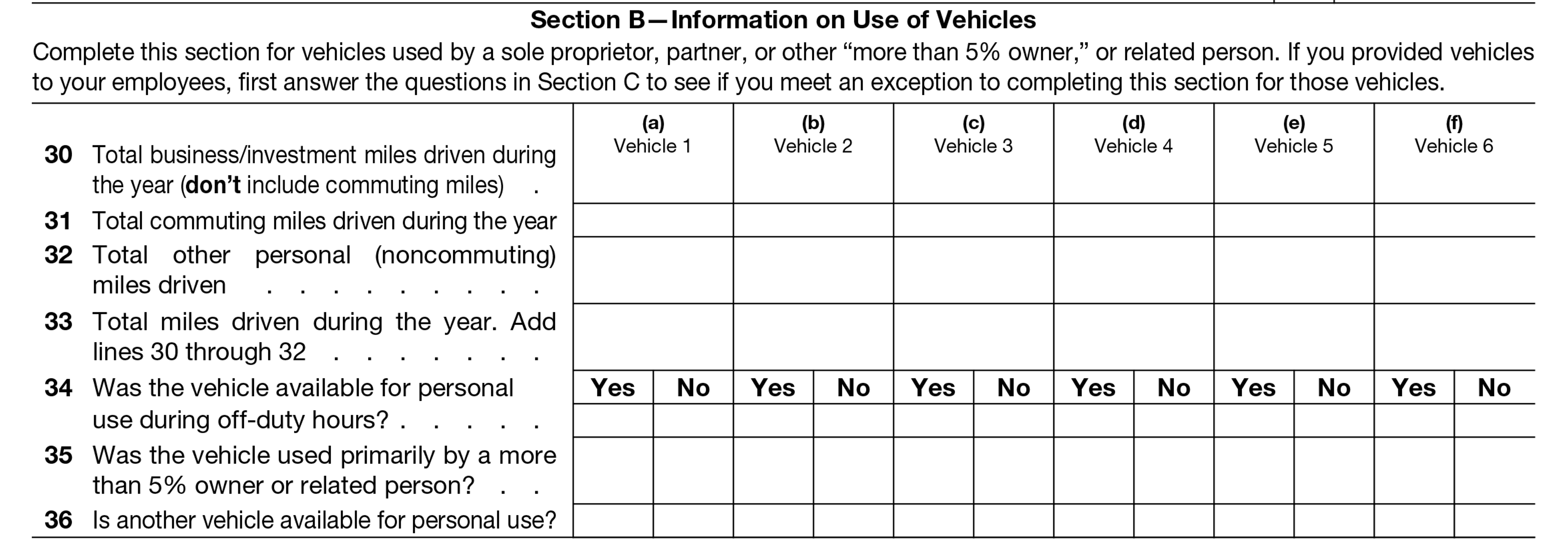

Section B—Information on Use of Vehicles

Use columns a-f in this section to provide additional information for any vehicles you’re claiming depreciation for, including total business miles (line 30), total commuting miles (line 31), total personal miles (line 32), total miles in general (line 33).

Use lines 34-36 to answer a series of Yes/No questions about whether the vehicle was available for personal use outside of work hours, whether the business owner used the vehicle, and whether there are vehicles other than this one available for personal use.

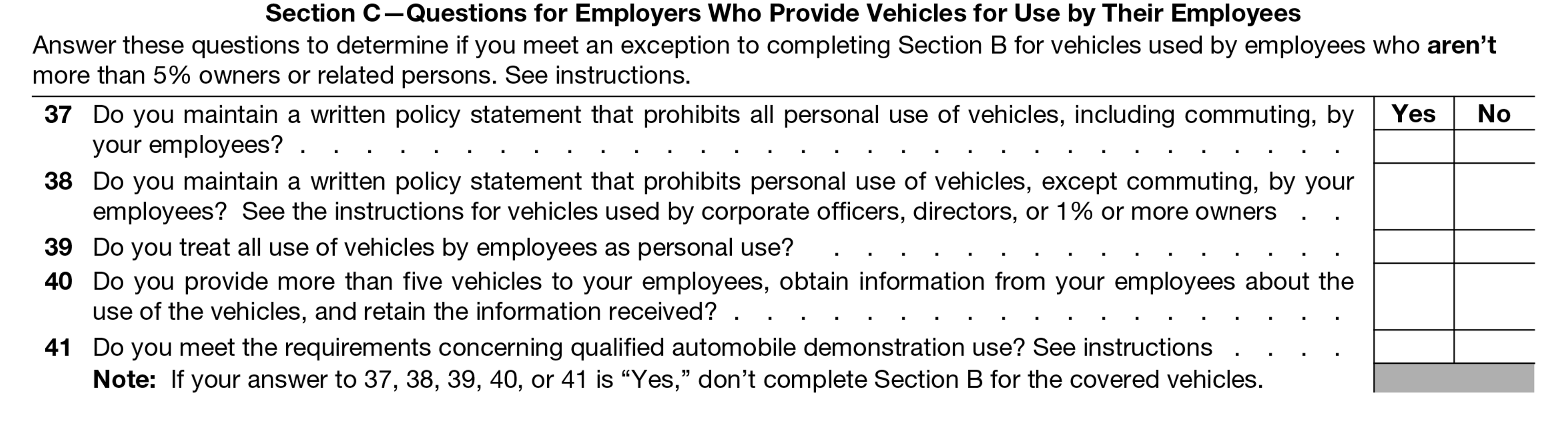

Section C—Questions for Employers Who Provide Vehicles for Use by Their Employees

If you employ drivers or other employees who use your business vehicles, use lines 37-41 to answer a series of Yes/No questions about your organization’s policies regarding the personal use of vehicles. If you answer “Yes” to any of them, don’t complete Section B for those vehicles.

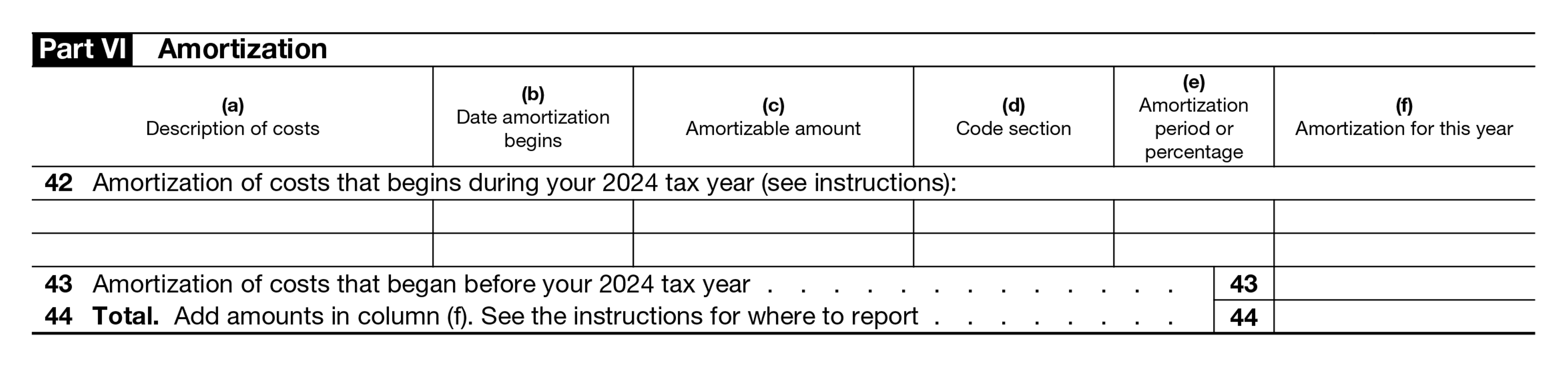

Part VI: Amortization

Use lines 42-44 and columns a-f to record amortization for intangible assets placed into use this year (line 42) and previous years (line 43) to come up with a total amortization amount (line 44).

Make Taxes Less Taxing With Ambrook

Ambrook’s category tags correspond directly to each line on Schedule F, making it easy to compare your tax return to your records and saving you hours of work during tax season.

With time-saving bookkeeping automation features, automatically-generated financial reports, streamlined bill pay and invoicing, and other powerful accounting and financial management tools, Ambrook doesn’t just make filing your taxes easy: it takes the guesswork out of running your business. Want to learn more? Schedule a demo today.

This resource is provided for general informational purposes only. It does not constitute professional tax, legal, or accounting advice. The information may not apply to your specific situation. Please consult with a qualified tax professional regarding your individual circumstances before making any tax-related decisions.